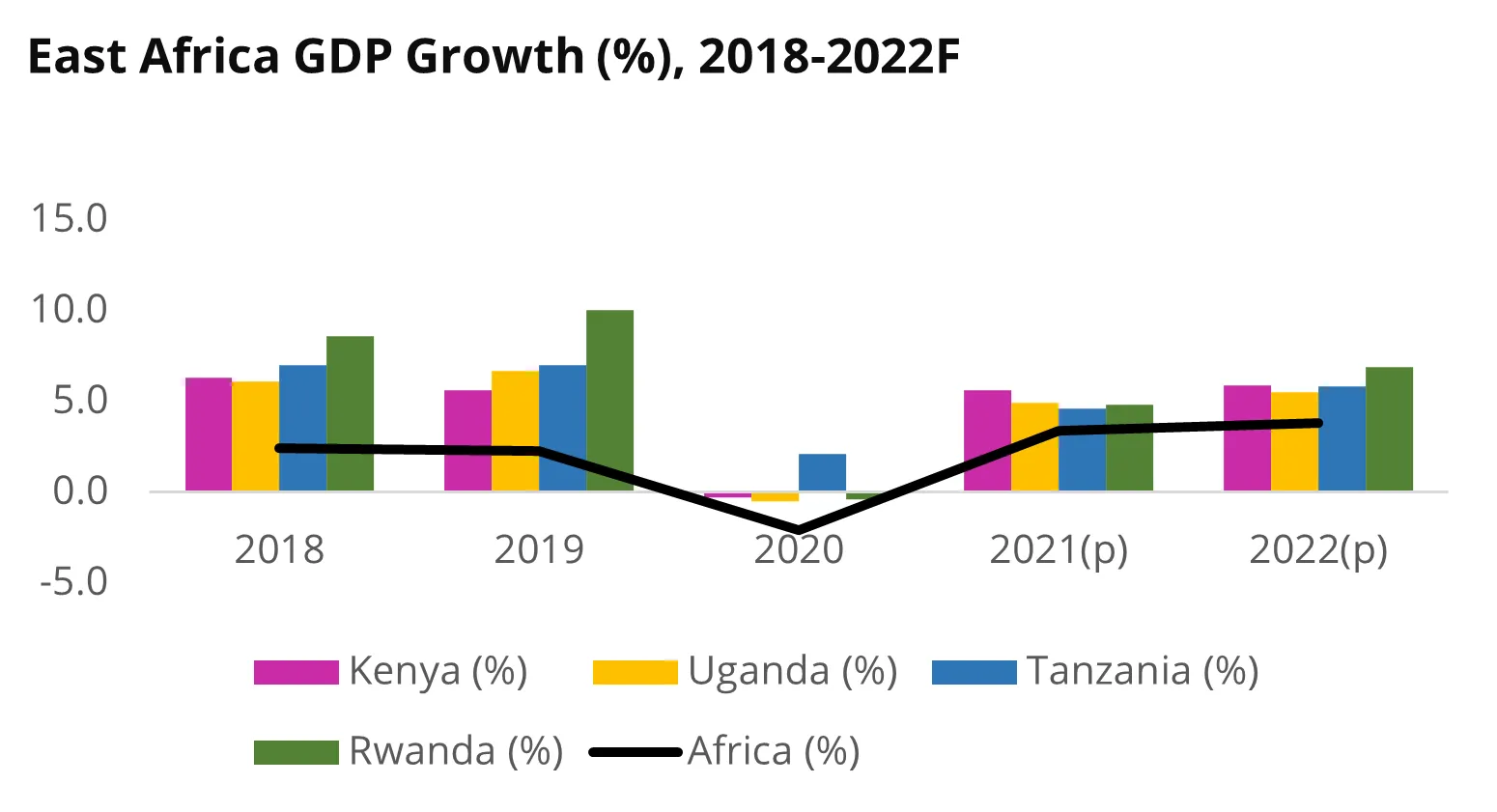

The resilience was driven by their low commodity dependence, large informal sector activity coupled with an entrepreneurial culture, and relatively stronger penetration of digital technologies within more diversified economic sectors that allowed business activity and transactions to continue despite safety restrictions. These traits have signalled to a strong rebound for growth in the years post-pandemic and beyond with many market experts projecting growth in excess of 5% for all the economies of East Africa over the medium term. [3]

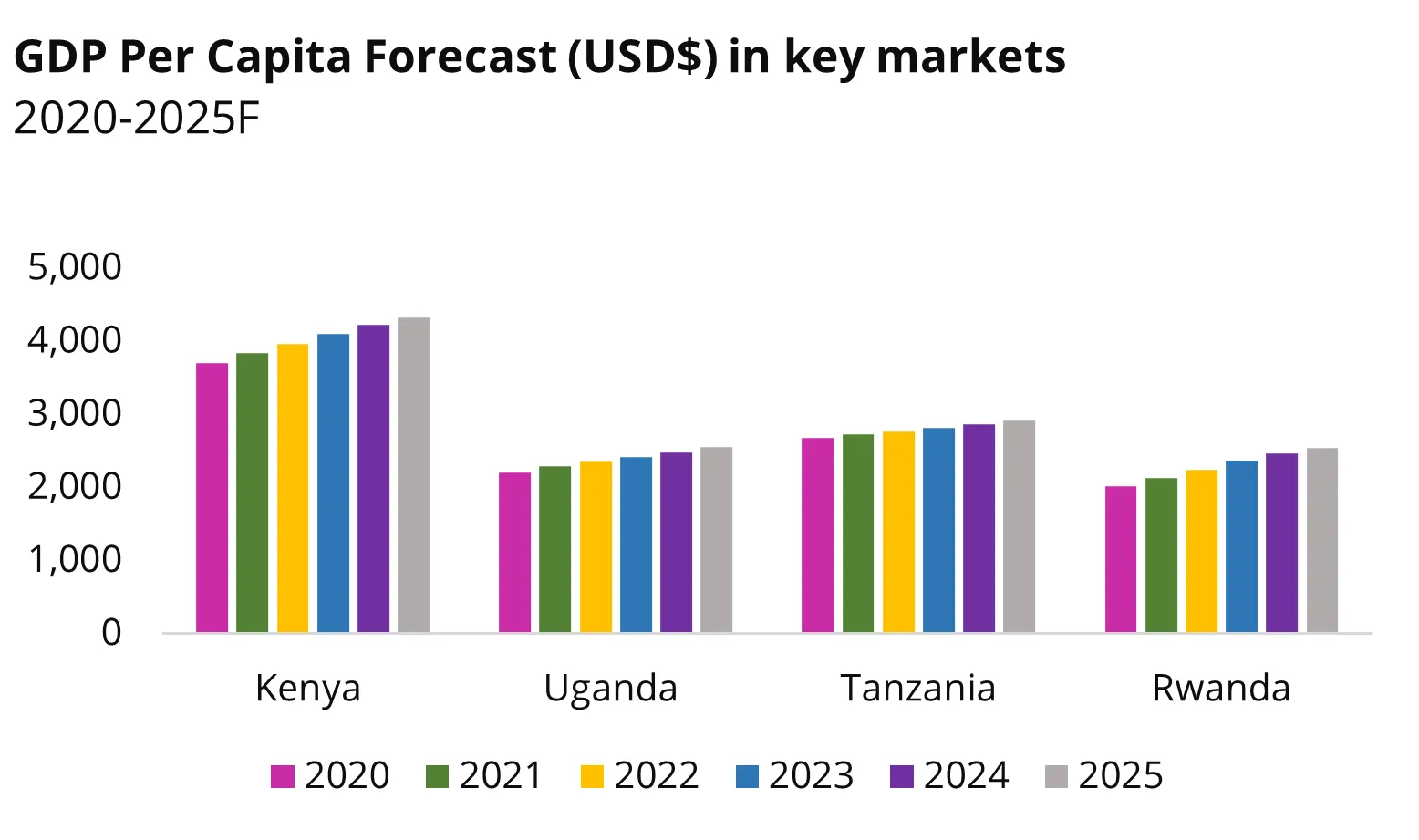

Many experts project that growth in this region will continue to accelerate steadily in the long-term, as demonstrated below:

The World Bank Group has retained Kenya’s growth projection at 5.5 per cent for 2022 in its latest country economic update [5] against economic shocks. The multi-lateral lender has also retained its outlook for 2023 and 2024 at 5 per cent and 5.3 per cent, respectively, the same rate as in June 2022. World Bank expects growth to be anchored on improved private consumption and gains on fiscal consolidation even as shocks, including drought, rising inflation and tighter global financing conditions.

Global leaders and delegates at the COP27 conference earlier in November 2022 have been warned of the addiction and dependence on fossil fuel. There is broad consensus that the emission of gases produced by fossil fuels must be dramatically cut by 2030 to keep the global temperature rising to 1.5 degrees and to avoid the most damaging effects of climate change. Russia’s invasion of Ukraine has also disrupted the markets and geopolitics of energy. In Kenya, this has also manifested itself as an increase in fuel prices leading to inflation hence a higher cost of living.

A section of Kenyans has had to make do with loans to purchase food as the cost of living soars significantly, driven primarily by high food prices. According to a survey by the World Bank [6], 12 per cent of households in Kenya have resorted to taking out loans to purchase food in the face of food price shocks whilst 34 per cent of households have meanwhile reported making purchases on credit in the face of shocks.